August 2025

Story 1: Gaming Ban

The Indian Government banned real-money games under the Promotion and Regulation of Online Gaming Bill (2025). [Link]

It doesn’t matter whether it is a game of skill or game of chance… if the game involves people adding money to win money then it is banned. Offering, facilitating and advertising such activities will attract severe penalties (fines and/or jail term).

There are two sides to this story:

Side A: Loss of jobs, Loss of GST revenue, investors lose trust in Indian startups etc.

Side B: Loss of money, mental health and life, Financial crimes, Terror financing etc.

As you know, GoI was on side B and passed the bill in both the Houses.

Apart from gaming merchants, the ban will impact many PAs and FinTechs as ‘gaming’ is one of the profitable sectors. Apart from payin, gaming merchants use payout, penny drop and PAN validation solutions from PAs/FinTechs.

This ban will impact celebrities; Not a big concern as they can still promote Paan Masala :)

Sometimes you win and sometimes you lose… and I am sure no one knows this better than these gaming merchants.

Many of these gaming merchants have big cash in their account and have smart people on their payroll… I am sure they will pivot and build something new. Good luck to them!

I. NPCI Realm

A. Things came into effect from August 1st

After the UPI downtimes in April, NPCI issued a circular in May '25 to reduce the over usage of API calls, reduce non-financial activities during peak hours, and many other things. [Covered in this article.]

NPCI had imposed restrictions on usage of following API calls:

Balance Enquiry

List Keys

List Account

Autopay mandate execution

List verified merchants

Penny Drop

ValCust

Validate Address

The changes to these APIs came into effect on 1st August.

B. UPI Limits increased

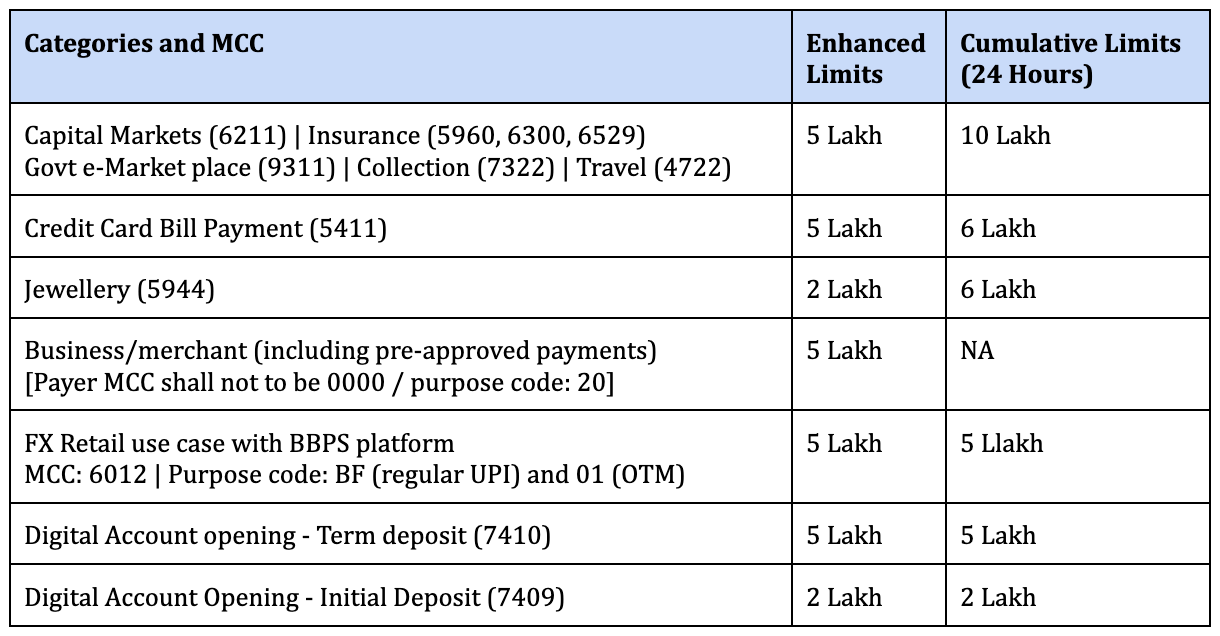

NPCI issued circular to enhance the limit of UPI P2M transactions [Link]

Deadline: 15-Sep-205

Applicable only for ‘verified merchants’

Banks may enforce their internal limits within the prescribed limits

C. Stopping UPI P2P Pull payments

NPCI is planning to stop the P2P pull payments by 1st Oct 2025. [link]

UPI works in two types of flows

Push: A person can transfer money to other person (by QR scan, to mobile, to VPA, to account number)

Pull: A user can send a collect request to another user and the payer will transfer funds.

In 2019, NPCI had enforced a limit of Rs.2000 for P2P pull payments.

Considering the frauds/scams, NPCI has decided to completely stop the pull payment.

Pull (Collect) payment will remain same for P2M (merchant payment)

D. PA + COU combo - What about Interoperability?

‘Interoperability’ is the cornerstone principle of India’s payment platforms. NPCI has championed the products such as UPI, FasTag, NACH etc.

The Bharat Connect (Erstwhile Bharat Bill Payment System) is another such interoperable platform. [Read this article to know the details of BBPS]

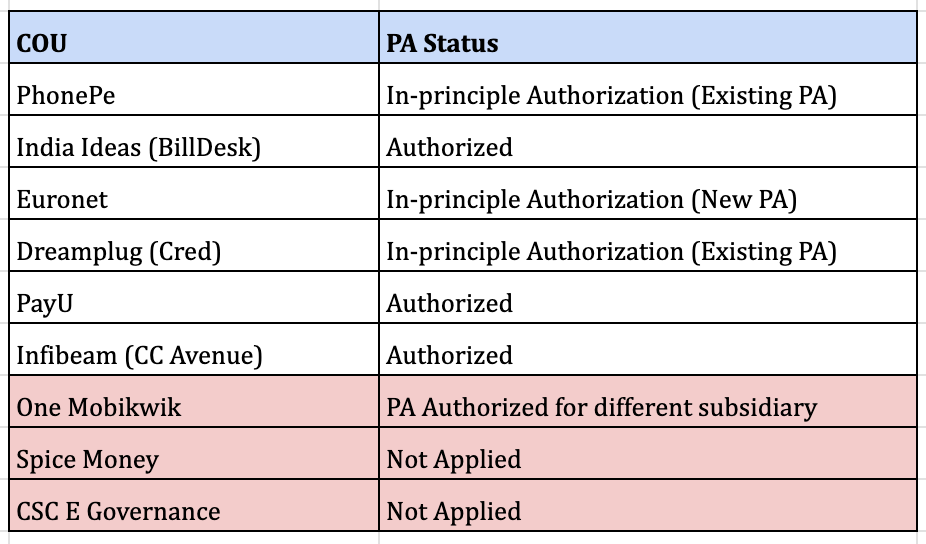

This month NBBL issued notice based on RBI’s guidelines [Link]

Agent Institutes to route BBPS transactions through COU and the same COU should act as the Payment Aggregator to process the customer transactions.

Although the idea is to stop the fragmentation in transaction flow, NBBL/RBI is taking away the flexibility of the Agent Institute.

Also, there are many unanswered questions

What will happen if the OU is down during bill payment?

If the digital agent institute is using a bank for UPI then who can be the OU?

Will RBI instruct sponsor banks to reduce NDC limits as risk is lower?

Any authorized PA can become BBPOU (BOU and/or COU) based on acknowledgement mail from RBI (no separate authorization needed).

All significant non-Bank COUs have PA license or in-process of getting one except the highlighted ones.

PA+COU combo will come into effect by 30th June 2026.

Winners: PAs (as they can push their COU and make extra revenue)

Losers: BillDesk (may lose volume), Agent Institutes (need to manage two PA+COUs and pre-funding them, lose flexibility to use preferred PA for processing payments)

II. RBI Realm

A. FREE-AI

Today, you won’t miss three things in a day - pot holes on road, QR code in store and AI talks in office.

“AI is not the future, it is happening now” (Tip: Deeper the voice, better the impact… Try it)

AI is everything and everywhere - it is a productivity tool for people who want to be productive, it is a laziness tool for those who want to be lazy, it is playground for people who likes to experiment, it is distraction for leaders who do not vision, it gave artificial reason for companies to layoff people, and it is time pass for people who have time.

It's remarkable how companies, products, and even individuals have overnight become "powered by AI."

AI will definitely impact us… including the payments.

So, RBI published the Framework for Responsible and Ethical Enablement of Artificial Intelligence committee report. [Link]. In short, FREE-AI (I hope people won’t think that RBI will give free access to AI tools).

It is a 90+ page report, I am not going to summarize it in this post (may be will write a separate article on it). Meanwhile, you can read here or use an AI tool to summarize it.

B. Faster clearing of Cheques

Cheques are quite interesting - There are 9 different types of Cheques and 90 different reasons for cheque clearance failure! [If you are interested then read this article]

For those who do not know - Cheques are documents issued by the bank that can be used by the payer to make payment of a specific amount to the payee or the bearer.

RBI is introducing Continuous Clearing and Settlement on Realisation in Cheque Truncation System (CTS) with the intent of reducing clearance of cheques from present T+1/T+2 days to a few hours. [Link]

The implementation would be done in two phases

Phase 1 (4-Oct-2025 - 2-Jan-2026): Drawee cheques will be cleared by 7PM on the same day; if the drawee bank doesn’t confirm by the cut-off time then such cheques are deemed approved

Phase 2 (from 3-Jan-2026): Drawee banks to clear the Cheques in T+2 hours (i.e. cheque that is received by drawee bank between 11AM-12PM to be cleared (approve/rejected) by 2PM.

Why take so much trouble for Cheques? Are they even relevant when we have NEFT and RTGS?

Cheques do have substantial volumes. In FY 2024-25, NPCI’s National Grid has processed 16.7Lakh cheques of value Rs. 19.5K Crore per day (Yes, per day).

C. Rupee Account

In 2022, RBI allowed opening of ‘Special Rupee Vostro Account (SRVA)’ that will allow cross-border trade settlement in Indian Rupees. [Link]

Authorized Dealer banks needed to take approval from Foreign Exchange Department of RBI.

Banks of 22 countries have opened SRVAs.

One of the issues with holding funds in INR is that the entities didn’t have ways to utilize the surplus.

See, if you have a US dollar surplus then you can use USD to make payments for other trades as USD is widely accepted.

This month RBI made two important changes [Link]

Special Rupee Vostro Account can be opened without the approval of RBI

The surplus amount can be invested in Central Government Securities

India has been on the path of internationalizing UPI, RuPay, technology behind UPI and Indian Rupee [Read this article].

D. Fines and Penalties

This month, RBI has imposed a total penalty of Rs.175.36 Lakhs on 28 entities.

Rs.54.56 lakh penalty on 24 Co-operative banks

2 NBFCs are fined with Rs.1.1 lakh

Rs.75 Lakh penalty on ICICI Bank and Rs.44.70 Lakh penalty on Bandhan Bank

III. Payment Entities/FinTech Realm

A. PA - Online

No new entity received a PA license this month. So the number of authorised PAs remains at 55.

Couple of big things happened in this space

PayTM Payments Services Limited received in-principle authorization and RBI lifted the embargo. After almost 2 years of embargo, PPSL can start onboarding new merchants.

Two interesting entities received in-principle authorization; IRCTC Payments Limited (a subsidiary IRCTC Limited) and Aditya Birla Capital Digital Limited.

Both are not core payments companies but can leverage their motherships to begin with in this ultra competitive payments business.

As new PAs, they can start PA operations only after receiving final authorization from RBI.

C. Other News

SEBI Clears Groww for IPO

Kiwi (UPI TPAP that centers around RuPay credit card linking) raised $25 Million

TransBnk (banking API provider) raised $25 Million

Sumitomo Mitsui Banking Corporation (Japan) has received RBI’s approval to acquire up to 24.99% of Yes Bank

V. International

A. Visa shuts open banking in USA

Visa has shut down its open banking services in the USA.

Reason: Uncertainty around customer data and fees to access the data (Banks may levy hefty fees on FinTechs/Open banks to access their customer data).

Talking about Open Banking, India also had a boom of open banks in 2019-2022. Many open banks started and raised funds. Even the BaaS (Banking as a Service) boomed along with that. Off lately, I haven’t heard much about these businesses. Was it just a fad and now, we have found a new one (e.g. AI)?

Story 2. US increased tariff on India

The US has imposed a tariff of 50% on goods imported from India.

The USA is one of the biggest importers of Indian goods (~20%) and contributes 2.2% of India’s GDP. The impact of high tariffs will impact Indian exporters and GDP growth (~0.7%).

Of course, GOI is taking various actions such as diversifying export destinations and reducing GST to boost domestic growth etc.

But one thing is clear, geopolitics is strange and it may play against you at any time. It is extremely important for us to be self reliant and diversify to reduce dependencies.

That's the wrap of August 2025!

[Read, subscribe, share]